To continue in the vein of my previous post on EMH, here’s an excerpt from a book

[1] I’m reading on volatility trading:

“Those sellers using local volatility models will certainly value a digital cliquet

[2] at a lower price than sellers using stochastic volatility. Perversely then, those sellers using an inadequate model will almost certainly win the deal and end up short a portfolio of misvalued forward-starting digital options, or even worse - a dealer could have an appropriate valuation approach but be pushed internally by the salespeople to match (mistaken) competitors' lower prices."

Basically – when you’re trading really complex structured derivatives nobody knows what the real price is, because said price can only be derived by a model and the models are largely proprietary. It’s arbitrary arbitrage! Without set market prices there can be no market efficiency.

Oh, but these are OTC derivatives Fama would say. To which I will reply that 1. you, kind sir, have already implied that there should be no measurable difference in efficiency when liquidity is decreased and 2. said derivatives are based on a very liquid equity option that is itself a derivation of allegedly perfectly efficient securities like equities, bonds and even currencies. Moreover, the mere fact that you cannot price these instruments without making predictions (discrete or not) about their future value means that option markets cannot be played passively on assumption that they are efficient.

At this point Fama would rise from his armchair and, thrusting his cigar at me in a decidedly confrontational manner while swirling his brandy irately, exclaim: “So am I to understand then, that you have no faith at all? No belief in market efficiency? Then I put it to you, sir, that you are a heretic of the first degree!”

To this I shall reply, while serenely sipping my single malt, “No, my friend – I am a heretic of the second degree. A heretic derivative, if you will, which is to say a rebel against theory, fighting in the name of reality. Indeed, just as you don’t advocate strong-form efficiency I in no way support the weak-form hypothesis. Moreover, I believe that news is priced very quickly (though not instantaneously) and that many (though not all) markets are mean-reverting. Nevertheless, inefficiencies exist and increase proportionately with a decrease in liquidity and regulation or an increase in complexity. Both technical and fundamental analysis can yield superior returns in the hands of a gifted (and not just lucky) individual. Some of us aren’t monkeys throwing darts at a list of stocks as your friend Malkiel believes. Rather, we are monkeys with sniper rifles. And we’ve got efficient markets in our sights.”

I then tip my hat to the bewildered Fama and make my exit. As Fama takes a sip of his brandy he realizes that ashes from his cigar have inadvertently fallen into the snifter. The taste is almost as raw as the state of his prized theory.

[1] The Volatility Surface: A Practitioner's Guide (Gatheral, 2006)

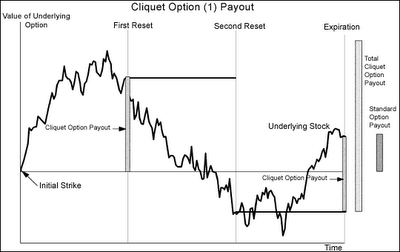

[2] From AMEX Dictionary of Financial Terms: The French like the sound of “cliquet,” and seem prepared to apply the term to any remotely appropriate option structure. (1) Originally a periodic reset option with multiple payouts or a ratchet option (from vilbrequin à cliquet—ratchet brace). Also called

Ratchet Option. See

Multiperiod Strike Reset Option (MSRO),

Stock Market Annual Reset Term (SMART) Note. See also

Coupon-Indexed Note. (2) See

Ladder Option or Note (diagram). Also called

Lock-Step Option. See also

Stock Upside Note Security (SUNS). (3) Less commonly, a rolling spread with strike price resets, usually at regular intervals. (4) An exploding or knockout option such as CAPS (from cliqueter—to knock)

Now that your are completely and utterly bewildered stare into this headlight young deer:

Ah, now it makes sense! It’s just a performance-linked digital option with resets! Duh.

This is CBS’ Credit Default Swap (CDS) curve. It widened over 25% yesterday - which means the bond market perceives a 25% increase in chance of default. This can occur for several reasons, one of them being when a company is about to undergo a leveraged buyout as the buyback of equity is financed with high-yield, less creditworthy “junk” bonds. Given that there have been no other credit-related rumors I suspect it’s an LBO signal.

This is CBS’ Credit Default Swap (CDS) curve. It widened over 25% yesterday - which means the bond market perceives a 25% increase in chance of default. This can occur for several reasons, one of them being when a company is about to undergo a leveraged buyout as the buyback of equity is financed with high-yield, less creditworthy “junk” bonds. Given that there have been no other credit-related rumors I suspect it’s an LBO signal. Now looking at the equity we see that it has been very strong in November and the trend is continuing. The lower graph shows that the MACD just crossed up over the signal. What this means is that there’s positive momentum on the equity that should continue. Nevertheless we haven’t seen a jump – perhaps because CBS investors are mostly cautious institutionals and want to wait to buy before there is a more confirmed rumor (or they may know something I don’t). In either case I‘d still buy at $32 as your risk/return is positively skewed – CBS won’t suddenly fall 20% like some penny stock as it is too big, but if there’s a buyout announced the equity should go up about 10-15%%. Just make sure to have a trailing stop of about 5% and you will be safe. Buy some out of money puts if you want insurance.

Now looking at the equity we see that it has been very strong in November and the trend is continuing. The lower graph shows that the MACD just crossed up over the signal. What this means is that there’s positive momentum on the equity that should continue. Nevertheless we haven’t seen a jump – perhaps because CBS investors are mostly cautious institutionals and want to wait to buy before there is a more confirmed rumor (or they may know something I don’t). In either case I‘d still buy at $32 as your risk/return is positively skewed – CBS won’t suddenly fall 20% like some penny stock as it is too big, but if there’s a buyout announced the equity should go up about 10-15%%. Just make sure to have a trailing stop of about 5% and you will be safe. Buy some out of money puts if you want insurance.

{kind=link}