One of Ambramovich’s more legitimate enterprises, Evraz Group SA, purchased Oregon Steel Mills for $2.3B, making it the biggest acquisition of a US company by a Russian one. I predict and hope this is the start of a trend. Why is this great news? Two reasons:

First, if Russians own American companies then the US can do the same shit to them that Russia does to its foreign investors. That is, coming up with phony violations and injunctions until the foreigners succumb to any and all demands. Not that any US party has the balls to actually do that outright, but it’s nice to know the possibility is there, and if American interests are oppressed far enough who knows what can happen. Anything that can possibly put a check on Putin’s despotic regime is a good thing.

Second, in order to buy out a public company or (better yet) take majority stake in a public company the buyer has to bare a certain amount of information. There is nothing better then thus subjecting Russian companies into exposing themselves, even if they’re only showing a leg. If this trend picks up the bra and the thong will come off soon enough. It’s a lot harder to trick/bribe the SEC (and US auditors in the wake of Sarbox) than the Russian government, so some Russian entities may actually have to clean themselves up to look presentable and legal. This would likely involve shaving some of the dirtier activities have heretofore been hidden from the public eye.

So even if I didn’t see these transactions as great opportunities for cross-border special situations arbitrage I welcome them, and hope they increase exponentially.

Wednesday, November 22, 2006

Monday, November 20, 2006

Litvinenko can't escape the KGB

Well it wasn’t Gazprom per se, but Russia’s mighty sickle has struck again – poisoning former FSB (Federalnaya Sluzhba Bezopasnosti or Federal Security Service) operative Alexander Litvinenko currently living (or, rather, dying) in London. The current incarnation of the KGB dubbed SVR (Sluzhba Vneshney Razvedki or External Reconnaissance Agency) stated “We have nothing to do with what happened to Litvinenko. The Russian secret services have not in a long time carried out poisonings or any form of assassination.” Well, obviously we wouldn’t expect them to outright admit it – denying obvious treacheries with rice paper thin cover ups is what Putin’s administration is all about. I mean, according to them Khodorkovsky (former CEO of OAO Yukos) is having a wonderful time in his Siberian prison (nevermind that he got sent to solitary for a week after the guards found he had some “unauthorized lemons” in his possessions).

Litvinenko, a critic of Russia’s policies, got sick immediately after a lunch with two SVR members. They were supposed to discuss Litvinenko’s investigation into the murder of a fellow dissenter - Anna Politkovskaya. One of the men was “Andrei Lugovoy, a former KGB bodyguard and one-time head of security at a television station owned by the Russian billionaire, Boris Bezerovsky” [telegraph.co.uk], whom Litvinenko knew – but the second man, as yet unidentified, was someone Litvinenko had never seen before. Berezovsky visited Litvinenko twice and agrees with the dying ex-agent as to whose hands are awash in blood.

A toxicology analysis found the culprit to be thallium, a colorless and odorless chemical similar in composition to salt. The former agent’s “bone marrow has failed and friends say he has visibly aged 20 years and lost all his hair. His immune system has been severely depleted and he has suffered severe kidney damage.” [gulfnews.com] Doctors say he has only a 20% chance of survival.

Litvinenko, a critic of Russia’s policies, got sick immediately after a lunch with two SVR members. They were supposed to discuss Litvinenko’s investigation into the murder of a fellow dissenter - Anna Politkovskaya. One of the men was “Andrei Lugovoy, a former KGB bodyguard and one-time head of security at a television station owned by the Russian billionaire, Boris Bezerovsky” [telegraph.co.uk], whom Litvinenko knew – but the second man, as yet unidentified, was someone Litvinenko had never seen before. Berezovsky visited Litvinenko twice and agrees with the dying ex-agent as to whose hands are awash in blood.

A toxicology analysis found the culprit to be thallium, a colorless and odorless chemical similar in composition to salt. The former agent’s “bone marrow has failed and friends say he has visibly aged 20 years and lost all his hair. His immune system has been severely depleted and he has suffered severe kidney damage.” [gulfnews.com] Doctors say he has only a 20% chance of survival.

Before and After:

Friday, November 17, 2006

Crapocalypse Now Redux

Check out this NYT article on G-Dub in Hanoi:

The story continues, however:

Yes – clearly defeat was an obvious option in Vietnam from the start. That is exactly what the administration said throughout that conflict. Oh wait, no – we lost sixty thousand soldiers believing in our just and infallible cause to democratize and liberate a foreign nation, and then eventually realized this may not have been such a hot idea. Whoops. Can we at least say we’re fighting for Oil or something else worth dying for? The people need a real material cause.

Mr. Bush spoke of driving by the lake where Senator John McCain’s plane crashed nearly 40 years ago, focusing less on Mr. McCain’s long imprisonment afterward than on the fact that “he was, literally, saved, in one way, by the people pulling him out.”Thank you so fucking much for “saving” Senator McCain, and by saving I mean:

On October 26, 1967, McCain's A-4 Skyhawk was shot down by an anti-aircraft missile, landing in Truc Bach Lake. He broke both arms and a leg after ejecting from his plane. After he regained consciousness, a mob gathered around him and stripped him of his clothing. He was then tortured by Vietnamese soldiers, who bayonetted him in his left foot and groin. His shoulder was crushed by a rifle butt. He was then transported to the Hoa Lo Prison, also known as the Hanoi Hilton. Once McCain arrived at the Hanoi Hilton, he was placed in a cell and interrogated daily. When McCain refused to provide any information to his captors, he was beaten until he lost consciousness. Alexander, Paul (2002). John McCain: Man of the PeopleMcCain, who unlike Bush, was an actual combat pilot and a damn good one at that, withstood torture upon torture in the name of his country, yet Bush is willing to dismiss all that by calling his captors saviors. I cannot even begin to tell you how disgusted I am by that.

The story continues, however:

For Mr. Bush, who had never set foot in Vietam before, this visit is something of a tightrope walk. America’s defeat here is increasingly being mentioned in comparison with how Iraq may turn out, and Mr. Bush was careful to stress that in Iraq, unlike Vietnam, defeat is not an option for the United States.

Yes – clearly defeat was an obvious option in Vietnam from the start. That is exactly what the administration said throughout that conflict. Oh wait, no – we lost sixty thousand soldiers believing in our just and infallible cause to democratize and liberate a foreign nation, and then eventually realized this may not have been such a hot idea. Whoops. Can we at least say we’re fighting for Oil or something else worth dying for? The people need a real material cause.

I also like the statement that Stanley Kranow makes in the end:

The easy summation is that Vietnam began as a guerrilla war and escalated into an orthodox war — by the end we were fighting in big units. Iraq starts as a conventional war, and has degenerated into a guerrilla war. It has gone in an opposite direction. And it’s much more difficult to deal with.

We “won” the war in a matter of weeks. It was our incessant need to promote democracy and autonomy of the indigenous people rather than imposing strict martial law and a puppet dictator with an army of primarily local soldiers (and I hope by now the US has learned how to properly keep one restrained) that kept us there, suffering casualties as we try to gently pacify people who never wanted us there in the first place. Whichever party you affiliate with (although perhaps especially for us Libertarians) it's getting ever easier to lose faith in the government.

Wednesday, November 15, 2006

Who will Gazprom assasinate next?

After this cheeky bit of news:

Arkady Ostorvsky for making the below comment in his article in the WSJ:

"Gazprom, the dominant gas supplier that frequently doubles as a Kremlin foreign policy arm, is not producing enough for an economy growing at more than 6 per cent a year. "

Vladimir Milov, head of the Institute for Energy Policy, for making the following comment to the media:

"Gazprom was given enormous privileges in exchange for providing the country with gas at regulated prices. If it wants to behave as a commercial company, it should not be a monopoly."

German Gref, minister for economic development and trade for implying Gazprom should be “independently regulated.”

Analysts at UBS Russia for questioning Gazprom’s strategy.

The citizens of St. Petersburg as they re-experience the horrors of WWII when their city loses heat in the middle of winter.

The country of Turkmenistan for not supplying enough gas and quibbling with the Allmighty.

Chechnyan Warlords (or random Georgians who will be dressed up to look like Chechnyan warlords) who will then be blamed for the gas shortage as well as every other problem plaguing Russia at the moment.

Always seeking to profit from energy arbitrage, I am relocating some of my freelance monkey snipers (alluded to in the previous post) to Russia.

“The head of a Russian fund that says it promotes the development of small oilOne simply has to wonder - who will be next? Will it be…

and gas producers was shot dead on Tuesday in southwest Moscow, the Reuters news agency reports. Zelimkhan Magomedov, 50, general director of the National Oil Institute Fund, was shot twice in the head.”

Arkady Ostorvsky for making the below comment in his article in the WSJ:

"Gazprom, the dominant gas supplier that frequently doubles as a Kremlin foreign policy arm, is not producing enough for an economy growing at more than 6 per cent a year. "

Vladimir Milov, head of the Institute for Energy Policy, for making the following comment to the media:

"Gazprom was given enormous privileges in exchange for providing the country with gas at regulated prices. If it wants to behave as a commercial company, it should not be a monopoly."

German Gref, minister for economic development and trade for implying Gazprom should be “independently regulated.”

Analysts at UBS Russia for questioning Gazprom’s strategy.

“Analysts say the problem is not the lack of gas - Russia has 16 per cent of the world's total reserves - but rather Gazprom's investment strategy. Over the past few years the company has spent vigorously on anything but developing its reserves. It has built a pipeline to Turkey, taken over an oil company, invested in UES and tried to gain a foothold in European distribution markets. All this was in the name of creating a national energy champion. But investment in Gazprom's core activity was inadequate.”Why has Gazprom not been investing in developing fields? Because it’s going to take Sakhalin away from Shell (who has already done all the work).

The citizens of St. Petersburg as they re-experience the horrors of WWII when their city loses heat in the middle of winter.

The country of Turkmenistan for not supplying enough gas and quibbling with the Allmighty.

Chechnyan Warlords (or random Georgians who will be dressed up to look like Chechnyan warlords) who will then be blamed for the gas shortage as well as every other problem plaguing Russia at the moment.

Always seeking to profit from energy arbitrage, I am relocating some of my freelance monkey snipers (alluded to in the previous post) to Russia.

Monday, November 13, 2006

cliquer l'hypothèse efficace du marché

To continue in the vein of my previous post on EMH, here’s an excerpt from a book[1] I’m reading on volatility trading:

“Those sellers using local volatility models will certainly value a digital cliquet[2] at a lower price than sellers using stochastic volatility. Perversely then, those sellers using an inadequate model will almost certainly win the deal and end up short a portfolio of misvalued forward-starting digital options, or even worse - a dealer could have an appropriate valuation approach but be pushed internally by the salespeople to match (mistaken) competitors' lower prices."

Basically – when you’re trading really complex structured derivatives nobody knows what the real price is, because said price can only be derived by a model and the models are largely proprietary. It’s arbitrary arbitrage! Without set market prices there can be no market efficiency.

Oh, but these are OTC derivatives Fama would say. To which I will reply that 1. you, kind sir, have already implied that there should be no measurable difference in efficiency when liquidity is decreased and 2. said derivatives are based on a very liquid equity option that is itself a derivation of allegedly perfectly efficient securities like equities, bonds and even currencies. Moreover, the mere fact that you cannot price these instruments without making predictions (discrete or not) about their future value means that option markets cannot be played passively on assumption that they are efficient.

At this point Fama would rise from his armchair and, thrusting his cigar at me in a decidedly confrontational manner while swirling his brandy irately, exclaim: “So am I to understand then, that you have no faith at all? No belief in market efficiency? Then I put it to you, sir, that you are a heretic of the first degree!”

To this I shall reply, while serenely sipping my single malt, “No, my friend – I am a heretic of the second degree. A heretic derivative, if you will, which is to say a rebel against theory, fighting in the name of reality. Indeed, just as you don’t advocate strong-form efficiency I in no way support the weak-form hypothesis. Moreover, I believe that news is priced very quickly (though not instantaneously) and that many (though not all) markets are mean-reverting. Nevertheless, inefficiencies exist and increase proportionately with a decrease in liquidity and regulation or an increase in complexity. Both technical and fundamental analysis can yield superior returns in the hands of a gifted (and not just lucky) individual. Some of us aren’t monkeys throwing darts at a list of stocks as your friend Malkiel believes. Rather, we are monkeys with sniper rifles. And we’ve got efficient markets in our sights.”

I then tip my hat to the bewildered Fama and make my exit. As Fama takes a sip of his brandy he realizes that ashes from his cigar have inadvertently fallen into the snifter. The taste is almost as raw as the state of his prized theory.

[1] The Volatility Surface: A Practitioner's Guide (Gatheral, 2006)

[2] From AMEX Dictionary of Financial Terms: The French like the sound of “cliquet,” and seem prepared to apply the term to any remotely appropriate option structure. (1) Originally a periodic reset option with multiple payouts or a ratchet option (from vilbrequin à cliquet—ratchet brace). Also called Ratchet Option. See Multiperiod Strike Reset Option (MSRO), Stock Market Annual Reset Term (SMART) Note. See also Coupon-Indexed Note. (2) See Ladder Option or Note (diagram). Also called Lock-Step Option. See also Stock Upside Note Security (SUNS). (3) Less commonly, a rolling spread with strike price resets, usually at regular intervals. (4) An exploding or knockout option such as CAPS (from cliqueter—to knock)

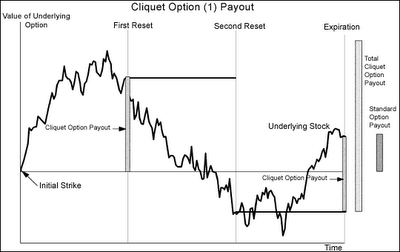

Now that your are completely and utterly bewildered stare into this headlight young deer:

Ah, now it makes sense! It’s just a performance-linked digital option with resets! Duh.

“Those sellers using local volatility models will certainly value a digital cliquet[2] at a lower price than sellers using stochastic volatility. Perversely then, those sellers using an inadequate model will almost certainly win the deal and end up short a portfolio of misvalued forward-starting digital options, or even worse - a dealer could have an appropriate valuation approach but be pushed internally by the salespeople to match (mistaken) competitors' lower prices."

Basically – when you’re trading really complex structured derivatives nobody knows what the real price is, because said price can only be derived by a model and the models are largely proprietary. It’s arbitrary arbitrage! Without set market prices there can be no market efficiency.

Oh, but these are OTC derivatives Fama would say. To which I will reply that 1. you, kind sir, have already implied that there should be no measurable difference in efficiency when liquidity is decreased and 2. said derivatives are based on a very liquid equity option that is itself a derivation of allegedly perfectly efficient securities like equities, bonds and even currencies. Moreover, the mere fact that you cannot price these instruments without making predictions (discrete or not) about their future value means that option markets cannot be played passively on assumption that they are efficient.

At this point Fama would rise from his armchair and, thrusting his cigar at me in a decidedly confrontational manner while swirling his brandy irately, exclaim: “So am I to understand then, that you have no faith at all? No belief in market efficiency? Then I put it to you, sir, that you are a heretic of the first degree!”

To this I shall reply, while serenely sipping my single malt, “No, my friend – I am a heretic of the second degree. A heretic derivative, if you will, which is to say a rebel against theory, fighting in the name of reality. Indeed, just as you don’t advocate strong-form efficiency I in no way support the weak-form hypothesis. Moreover, I believe that news is priced very quickly (though not instantaneously) and that many (though not all) markets are mean-reverting. Nevertheless, inefficiencies exist and increase proportionately with a decrease in liquidity and regulation or an increase in complexity. Both technical and fundamental analysis can yield superior returns in the hands of a gifted (and not just lucky) individual. Some of us aren’t monkeys throwing darts at a list of stocks as your friend Malkiel believes. Rather, we are monkeys with sniper rifles. And we’ve got efficient markets in our sights.”

I then tip my hat to the bewildered Fama and make my exit. As Fama takes a sip of his brandy he realizes that ashes from his cigar have inadvertently fallen into the snifter. The taste is almost as raw as the state of his prized theory.

[1] The Volatility Surface: A Practitioner's Guide (Gatheral, 2006)

[2] From AMEX Dictionary of Financial Terms: The French like the sound of “cliquet,” and seem prepared to apply the term to any remotely appropriate option structure. (1) Originally a periodic reset option with multiple payouts or a ratchet option (from vilbrequin à cliquet—ratchet brace). Also called Ratchet Option. See Multiperiod Strike Reset Option (MSRO), Stock Market Annual Reset Term (SMART) Note. See also Coupon-Indexed Note. (2) See Ladder Option or Note (diagram). Also called Lock-Step Option. See also Stock Upside Note Security (SUNS). (3) Less commonly, a rolling spread with strike price resets, usually at regular intervals. (4) An exploding or knockout option such as CAPS (from cliqueter—to knock)

Now that your are completely and utterly bewildered stare into this headlight young deer:

Ah, now it makes sense! It’s just a performance-linked digital option with resets! Duh.

Wednesday, November 01, 2006

Fama Keeps Preaching (but the choir ain't singing)

Fama, my old nemesis, is still preaching efficient markets. Check out the interview.

I especially love the interviewer’s interrogation regarding the 1987 crash, although I am disappointed she did not ask him about his own little fund, Dimensional, and its strategies. Namely how does Dimensional pick “risks that are worth taking and the risks that are not.”

Some parts I shall comment on:

(FEN - Financial Engineering News, EF - Eugene Fama, BSD - Arbitrageur's apropos pseudonym)

FEN: As an undergraduate at Tufts, you tried to beat the market.

EF: Yes. I was already working on stock market data. I tried to figure out ways to beat the market for Harry Ernst, who taught economics. I came up with mechanical kinds of strategies. He always made me have a hold-out sample to see if the strategy worked on new data – and it never did.

BSD: …and as a way of justifying your failure you dedicated the rest of the life to erroneously proving that you were playing a game one cannot win (although – of course – some consistently do).

FEN: If markets are efficient, a stock price reflects the intrinsic value of a company, but does that mean the price is always right?

EF: It means you can’t figure out whether it’s wrong. It’s not always right because there’s some uncertainty about what right is, but basically you just can’t beat it.

BSD: In another life you would have made a great spin doctor or lobbyist. You neither answered the question nor provided any evidence to the contrary of the point presented – you simply questioned the meaning of “right.”

FEN: What about [inefficiencies in] smaller, illiquid stocks?

EF: That’s what people claim – that smaller stocks are not priced as efficiently as bigger stocks, that emerging markets are not priced as efficiently as developed markets. But anyone who looks at it empirically can’t find any evidence to that effect.

BSD: Yeah, anyone but the investors who’ve been consistently raping those markets precisely on the basis of exploiting inefficiencies that result from a poorly regulated market.

FEN: I was just talking to a trader in Canada who’s at a fund that has beaten the broad Canadian market by investing mainly in financials for the last 20 years.

EF: Look across the spectrum of all funds – you’ll always find people in both tails. That can happen even if nobody has any special information. Some people are going to be lucky and some unlucky. The lucky ones get the attention, and then they think they’re smart.

BSD: So guys like Stevie Cohen who’ve been “lucky” for decades must have made some deal with the devil, because statistically such a streak of luck is near-impossible.

FEN: Have you moderated your views over the years that markets are efficient? Many academics and others say you have.

EF: Many people get confused. Many people don’t understand the difference between efficient markets and the risk-return story.

BSD: I think you don’t understand the difference, homey. Your original paper, understandably, does not account for the many ways to hedge risk that currently exist. The problem is that, like a caveman driving a car on square wheels you are unwilling to change.

FEN: There’s no need for active investors to go in search of information?

EF: There’s no need for active investors who don’t actually succeed in uncovering new information. People who act on bad information make prices worse.

BSD: Correct. So, since – according to you – most active managers act on bad information their very existence erodes efficiency.

FEN: Are traders following momentum strategies an example of people without information moving the market away from the most efficient price?

EF: I don’t know.

BSD: BS. You do know, you just can’t explain it with your theory. You said (in this very interview) that there is “evidence that there’s some short-term momentum in returns” – the very existence of observable and predictable momentum in liquid markets implies profit potential through an active strategy.

FEN: You’ve been a skeptic of the idea that people’s irrational behavior and decisions affect market prices in predictable ways, and you’ve been a critic of behavioral finance more generally. Do you think behavioral finance poses a threat to the idea of efficient markets?

EF: It poses interesting questions and legitimate questions for research. I haven’t seen researchers in that area come up with much that indicates that prices are bad. They’ve produced a lot that indicates that individual investors don’t always act completely rationally. Those are two different things. At the micro-micro level, they have done some really interesting stuff. At the level of price-setting, it’s not so clear.

BSD: Assuming a significant number of price-setters who do not act rationally how can markets be efficient? You cannot say that there is no direct relationship between price efficiency and the rationality of market participants. Furthermore, there has been research applying behavioral finance to prices – you just aren’t bringing it up, perhaps because you can’t outright disprove it.

Subscribe to:

Posts (Atom)

{kind=link}